uss life insurance

Up One Level

Life insurance coverage economically safeguards your family and other individuals who rely on your earnings. If you have life insurance coverage, it will make payments after your death to the individual you name in your policy. This person is called your recipient. You can name more than one beneficiary. Your beneficiaries can use the cash to pay bills and living expenses, settle debts, spend for college, and other things.

Not everyone needs life insurance. dave ramsey life insurance. In general, life insurance coverage is a good concept if you have household or others who count on you economically. There's no formula to decide just how much life insurance you require. To choose the quantity that's right for you, consider your financial obligations, the amount of earnings your family must replace, and whether they'll have expenses or other expenses.

Insurance coverage companies utilize a procedure called underwriting to choose whether to offer you a policy. This frequently consists of passing a medical exam and answering questions about your health, task, and practices (banner life insurance). A company can refuse to sell you a policy if it considers you a high risk due to the fact that of your health or other factors.

Texas Life Insurance Lawyers - Life Insurance

The underwriting requirements for group life insurance coverage isn't as rigorous. You normally do not need to respond to questions about your health. As an outcome, you may be able to get group life insurance coverage even if you aren't able to purchase directly from an insurer. The cost depends on your circumstances.

They're usually lower for younger people. They can be high if you're older or have danger elements. A company can charge you more if you smoke or have dangerous pastimes like sky diving or rock climbing. Your premium will also depend upon other things, consisting of the amount of protection and policy features you pick.

The expense is generally cheaper than for a policy you purchase straight from an insurance business - northwestern mutual life insurance. There are 2 main kinds of life insurance coverage: term life and long-term life insurance coverage. Term life insurance coverage offers defense for a set period of time. This period is called a term. The term can be for one year, or anywhere from 5 to 30 years or longer.

Texas Life Insurance Company Company Profile - Waco, Tx ... - Life Insurance Companies

Term life policies pay a swelling amount, called a survivor benefit, to your beneficiaries if you pass away during the policy's term. The policy ends at the end of the term, unless you pay to extend it. Term policies aren't indicated to offer protection for your entire life. The majority of people who buy term life policies want protection for only a time, such as while they're raising a household or have kids in college.

They'll increase if you renew at the end of the term. This is since your new premium will be based upon your age when you renew, not when you initially bought the policy. To help prevent higher premiums later on, consider buying a policy with a longer term. A lot of companies provide term life insurance coverage just approximately a particular age, generally 70 or 80.

They make it easier to get a various type of policy or keep the one you have. lets you exchange your term policy for a long-term life policy without needing to take a medical examination or answer questions about your health. This can be helpful if your health worsens after you buy a term policy.

Texas Life Insurance Company - Linkedin - Best Life Insurance

Business typically enable you to transform term life policies just for a time, usually until you turn 65. lets you extend your policy for additional terms, no matter your health and without needing to take a medical test. Long-term life insurance coverage lets you construct cost savings with time. You can withdraw from, invest, or obtain versus this savings.

A part of each of your premiums is put into an account, referred to as the cash worth. The cash worth grows at either a repaired or variable rates of interest. Some policies tie the development to indexes, such as the S&P 500, or to sub-accounts you select. The sub-accounts are invested in stocks, bonds, or both (lincoln heritage life insurance).

It takes a policy a number of years to develop a money worth. You may need to pay a surrender charge if you withdraw the money early. And if you withdraw more cash than you paid in premiums, you'll most likely need to pay taxes on it. If you withdraw the whole cash worth, the company may cancel your policy.

Texas Life Insurance - Accuquote - Aaa Life Insurance

Premiums for permanent life insurance are higher than for term life. That's because of the cost savings feature and since you're buying protection for a longer duration. But if you buy a permanent life policy when you're young and keep it, your premiums will likely be lower than for a term life policy you buy when you're middle-aged or older (what is whole life insurance).

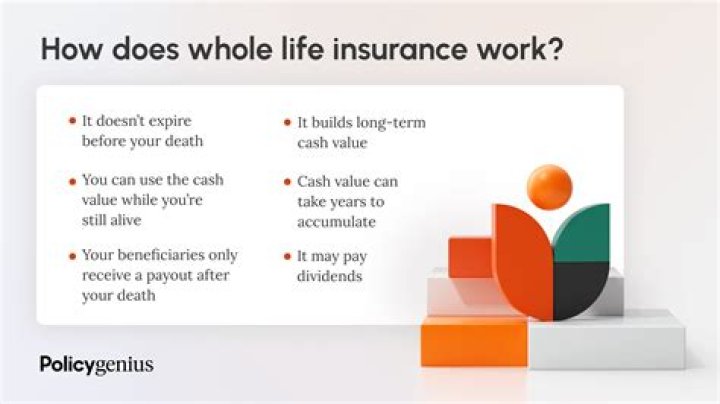

The 2 most typical kinds of long-term life insurance are whole-life insurance coverage and universal life insurance. stays in impact for your entire life unless you cash the policy in or stop paying premiums. Some whole-life policies might pay a dividend each year. You can get the dividend in cash, add it to your policy's money worth, or use it to pay premiums.

Your dividend might be lower than the company's projection. Prior to you purchase a policy, ask the company for a history of its predicted dividends versus paid dividends. northwestern mutual life insurance. stays in impact up until the maturity date, which is typically age 95 or 100, as long as you have $1 or more in cash value.

Texas Life Insurance Company - Complaints - Better Business ... - Term Life Insurance

Universal life insurance coverage is more flexible than entire life. You can change the amount of your premiums and death advantage. unum life insurance. However any modifications you make could impact how long your coverage lasts. If your premiums are lower than the expense of insurance, the difference is taken from the money worth.

The company will send you a report each year revealing your cash value and for how long the policy might last. The quote is based upon the money value quantity, the cost of insurance, and other aspects. Review it thoroughly. You might require to pay more in premiums to keep the policy in impact till the maturity date.

Variable universal life policies depend on the efficiency of the sub-accounts you select. Representatives who offer variable life insurance in Texas need to have a federal securities license and a state insurance license. Some universal life policies have a no-lapse assurance. If your premium payments aren't enough to cover the cost of insurance, the no-lapse warranty keeps the policy in effect.

Texas Life Insurance - Tx Life Insurance Quotes - Quickquote® - Gerber Life Insurance

Enjoy: Universal life: Your policy might be vaporizing Irreversible life Term life Entire life Universal life Low at very first but may go up each time you restore the policy - midland national life insurance. Premiums are based upon your age when you buy or renew your policy. Higher than term life at initially, but generally do not increase.

Versatile. Premiums are based upon your age when you buy the policy. Many policies let you alter your premium payments, but it will affect your survivor benefit, money worth, or both. The period you select, usually one year, five to thirty years, or longer. Your entire life if you keep the policy.

The policy stays in effect until the maturity date, typically at age 95 or 100, as long as you have a cash worth (is life insurance taxable). Death benefits only. Death advantages, plus a possible cash worth you can withdraw from, invest, or borrow versus. Death benefits, plus a possible cash value you can withdraw from, invest, or obtain against.

Texas Life Insurance Company - Crunchbase Company ... - Colonial Penn Life Insurance

You can convert to an irreversible life policy or renew without having to take a medical test. Premiums, survivor benefit, and money values are ensured. Versatile. You can change the survivor benefit and premiums. Premiums will go up each time you restore. Doesn't permit you to develop savings. May be expensive to cover a short-term need.

Not flexible adequate to make modifications when needed. Might be pricey to cover a short-term requirement. The payment isn't ensured. Low interest rates can affect cash value, which may increase your premiums - new york life insurance. These kinds of life insurance provide only specific coverages: pays the balance of a loan if you pass away prior to the loan is paid off.

If you already have life insurance, you may not need credit life. Instead, you can assign a few of the survivor benefit to the lending institution to pay the loan balance. pays your funeral service expenditures. An advantage of this insurance is that it locks in funeral expenses at existing prices. Funeral insurance coverage can be costly compared to other kinds of life insurance.

Understanding Life Insurance - Texaslawhelp.org - Providing ... - New York Life Insurance

And many policies will not pay the full expense of the funeral if you die prior to paying a required amount - ameritas life insurance. A routine life insurance coverage policy or savings may be a better method to pay for a funeral. You can generally include functions or other protections to your policy so it much better matches your requirements.

A few of the most typical riders are: adds term life coverage to a permanent life policy. For circumstances, if you need $500,000 worth of overall coverage, you might purchase a $100,000 whole-life policy with a $400,000 term life rider. As you make more money, you might transform the term life rider into a universal life policy or purchase an extra whole-life policy.

The business might still utilize these elements to pick your premium. You usually must purchase the extra protection by a defined date or life event, such as when you retire or prior to you turn 50. supplies an additional payment if you pass away since of a mishap. allstate life insurance. For instance, if you have a policy with a $500,000 survivor benefit and a $500,000 unintentional death rider, your beneficiary would get $1 million if you pass away because of a mishap.

Texas Life Insurance Co - Company Profile And News ... - Term Life Insurance

covers the premium if you meet the policy's definition of handicapped - prudential life insurance. This rider is typically just readily available to people more youthful than 60. prepays some or all of the death benefit while you're still living. You should have a terminal disease, defined illness, or long-term care disease. People typically buy this rider to help pay long-lasting care expenses in case they need them later on.

Generally, this rider combines 2 policies into one. provides term life insurance for your children. A lot of business need the child to be a minimum of 14 days old. Protection generally lasts up until the kid turns 21 or 25. Some companies and other groups use life insurance coverage as a perk. Those that do need to make it readily available to all their staff members and members no matter age or health.

The amount of coverage is often minimal. A basic group policy through your job typically has a death advantage equal to one or 2 times your yearly income. Other group policies cap the death benefit at a set quantity, such as $100,000 for a term life policy and $50,000 for long-term life.

Texas Life Insurance - Tx Life Insurance Quotes - Quickquote® - Guardian Life Insurance

If you get life insurance coverage through your employer, coverage typically ends when you leave your job. Business usually pay the death advantage as a single lump amount, but there are other options. genworth life insurance. Either you or your beneficiary chooses how the death benefit will be paid. Typical alternatives consist of: The insurance provider keeps the death advantage and pays the interest to your beneficiary at regular intervals.

The insurance coverage business pays a set month-to-month total up to the recipient for the rest of his/her life. Under this alternative, the beneficiary might get more than the policy's specified survivor benefit if she or he lives longer than anticipated. Companies must pay the survivor benefit within two months after getting proof of death and confirming your beneficiary.

Companies might take longer to pay the survivor benefit if you pass away throughout the policy's contestable period - life insurance. Life insurance coverage policies have a two-year contestable duration. If you pass away within this duration, the business might review the details you offered on your insurance coverage application. If the business discovers you offered incorrect info or didn't divulge something, it can reject payment.

Back Next Article

Other Resources:

guaranteed reserve life insurance

covita life insurance

aurora national life insurance

no physical term life insurance